Want To Be a 10X Better Investor Than 90% Of People?

Use Warren Buffett's 3 Principles

Use Warren Buffett's 3 Principles:

1. Only invest in companies that you understand, and where you can reasonably estimate the future economics 10+ years out. That should eliminate most companies for most people.

Here is an example of one such company for me. A glass bottle manufacturer. The product has been around for a very long time. Demand is stable. There are substitutes, such as aluminum cans and plastic bottles, but share shifts are very slow. Capacity takes a long time to bring on stream. It’s a small portion of the total cost of the end product but important to how the end consumer perceives it. It is unlikely that a new alternative will be invented any time soon, and even if it were, there are both perceived and real switching costs.

Here are examples of companies that don’t pass this test for me: An early-stage biotech company working on a new drug. An electric vehicle manufacturer that has a strong brand but with a lot of competition and an industry with a history of many an exciting company having fallen by the wayside. A commodity producer whose long-term economics are dependent on the price of a commodity that I can’t confidently estimate.

The specifics aren’t as important as that you are comfortable with the answer. You might be quite happy estimating the economics of a company that I or someone else might pass on. As long as your confidence is based on insight and an honest self-assessment rather than on hubris, that’s totally fine.

2. Feel comfortable doing nothing most of the time. Good ideas are rare. The math of waiting is very forgiving - you can get 0% for a while and still have a good long-term rate of return as long as you have high returns when you do invest. On the other hand, it's hard to have a good rate of return if you have large losses.

Let’s say that you have two choices. You can earn 0% on your money for 3 years, after which you are going to invest it at a 15% annualized rate of return. Or you can invest it right away at a 7% annual rate of return. The first choice is meant to represent you not being able to find a sufficiently good idea for the first 3 years of looking – a fairly unlikely, but possible, scenario if you know where and how to look.

You can of course disagree with the assumptions. A 15% rate of return with moderate risk isn’t easy to find, right? Well, that’s the point. Good things are worth the wait. On the other hand, the 7% assumption is somewhere in the neighborhood of what the current, early-2023 U.S. stock market seems to offer on a long-term basis. Some would argue that’s even an optimistic interpretation of the current price levels.

Also, if instead of needing 3 years to find a 15% annual return idea it takes you only 2, then the 10-year annual rate of return becomes 12%, a full 5% per year above settling for being invested in sub-par returning investments. That’s a more realistic amount of time needed to find a good investment, and so I will use that as Scenario 1 going forward.

Let me be clear: I am not advocating market timing. Market timing is when someone says something like “gee, I think the market will go down a lot this year, so I am going to sit on the sidelines.” This isn’t that – it’s absolute value investing, as opposed to relative value investing.

We are simply saying that we have a minimum hurdle rate that we require in order to invest. If an investment meets that hurdle rate as well as our qualitative requirements, then we invest, regardless of what the market may or may not do. If we don’t find enough ideas that meet our absolute return threshold, we wait until we do. So waiting or investing isn’t a function of our opinion about what stock prices will do, it’s a residual of our valuation discipline.

Let me add one more scenario. In this case, you start investing in a 7% annual rate of return investment and receive that return for the first 4 years. However, in year 5 something goes wrong and you end up with a big, 40%, loss. That, by the way, is not that different than what we saw some of the more, shall we say, adventurous investors achieve in 2022.

Having learned from your mistake you find religion and only invest in 15% annual rate of return investments going forward (years 6 through 10). Unfortunately, the math of big losses is unforgiving: your 10-year annualized rate of return falls all the way to 5%:

3. Demand both quality and a margin of safety. Many people dive in when they identify a high quality company. Others rush to buy really cheap stocks. The trick is to wait for both quality and a large discount from intrinsic value. You say that's very rare? Yep. See #2 above.

It’s fun and easy to own good companies. What can go wrong? You can boast about owning household brands. They are at the top of the “best places to work” lists. CEOs are on the cover of Fortune. And so on.

Sorry to spoil the fun, but there is a little problem. Usually you are not the only person who has figured out the magnificent quality of these companies. In many cases, the quality is so apparent that people are actually willing to accept below-average returns for the privilege of owning their shares. So it’s quite possible that you are exactly right on the quality of the business and management, but still achieve average or below-average returns.

The next time you see someone with a portfolio chockful of glamorous blue-chip names, just ask yourself this question: how likely is this person to have a meaningfully differentiated view on the long-term future of not just one, but 20-50 of these well-known and well-followed companies?

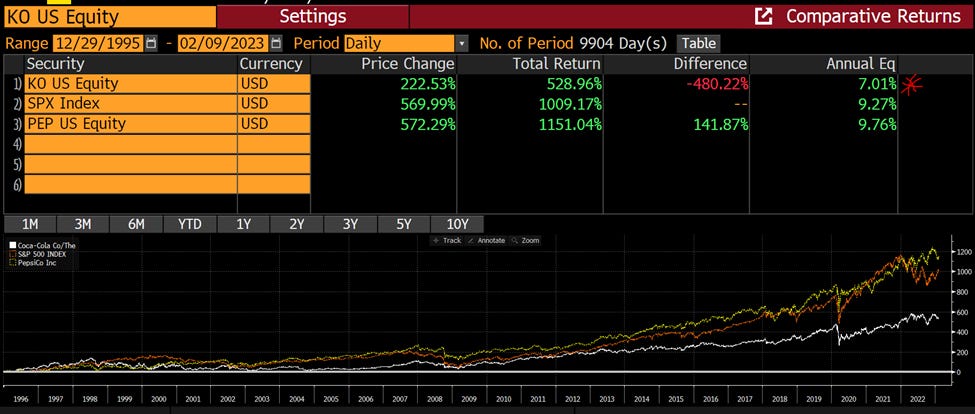

Here is how hard this is. Remember Warren Buffett? Well, he astutely bought Coca-Cola, one of the best companies in the world, very early on. And he did quite well for a while. Unfortunately he held on to that investment well past when he had any really differentiated view about its future. Below is a chart comparing the stock’s return since the beginning of 1996:

It has had dismal returns over a quarter of a century! This is despite the fact that its brands are still extremely strong, its products have grown, and so forth. Incidentally, I am not cherry-picking some specific starting point to help my argument. You can change the starting point to any number of years and the conclusion wouldn’t change. Quality without regard to valuation is just not very likely to work out well in the long-term.

So if valuation is the key, we should dive in and put together a portfolio of the cheapest stocks that we can find, right? Wrong! All “cheapness” means is that the price is low relative to what the company has earned in the past or relative to its assets. It says nothing about whether that cheapness is warranted or not.

Early in my career, I found a specialty chemical company that was really cheap. I estimated its mid-cycle normalized Earnings per Share (EPS) to be about $2.50. This was supported by its historical earnings and a thorough analysis of the company’s fundamentals.

The stock was trading at $22, or about a 9x P/E ratio. I figured it to be about an average company worth 15x * $2.50 or $38. $22 divided by $38 was under 60%, so I was good to go! I channeled my inner Benjamin Graham and recommended we buy this company’s stock as a good value investment.

One small problem. The actual future mid-cycle earnings ended up being… about 25c! So the next time you sweat a nickel or a dime in your estimates, think about being off by a factor of 10. That’s pretty humbling.

A big reason to demand quality in your investments is to substantially reduce the likelihood of being materially wrong in your long-term forecasts. The major reason to demand a big margin of safety is so that you can still earn a high return if everything goes according to plan and not do too badly if things go astray.

Let’s go back to the beginning. How can doing these 3 things help us achieve 10X the returns of 90% of people? Well, let’s start with the latter.

The average person is likely to invest in a mutual fund. That fund is likely to do about market minus fees. Let’s say 9.5% for the market (history over the last century is 9% to 10%) and so 9% for the mutual fund after fees.

There is a catch. The sad fact is that the average mutual fund holder underperforms the average mutual fund by anywhere between 2% and 6% per year according to studies. Why? They chase trailing performance, buy high and sell low. The industry unfortunately tacitly encourages such behavior with its cynical marketing tactics. So let’s say that the average fund holder is going to get a 6% annual rate of return.

If you take $1 and compound it at 6% per year for 40 years, you end up with about $10. If instead you compound at 12% per year, as in Scenario 1, you end up with $93. So not quite 10X, but I hope you will forgive me since it’s pretty darn close.

If you liked this article, please “like” and share this article.

About the author

Gary Mishuris, CFA is the Managing Partner and Chief Investment Officer of Silver Ring Value Partners, an investment firm that seeks to apply its intrinsic value approach to safely compound capital over the long-term. He also teaches the Value Investing Seminar at the F.W. Olin Graduate School of Business.

I think you meant 100x.

Super nice article. Thank you