The Adventures Of Mr. Stock Pickens McPickens

McPickens is one insightful hombre, and he is going to find that winning stock even in a tough market.

Currently, the ~1,000 quality companies that are my primary hunting ground are trading at an average normalized forward Free Cash Flow (FCF) yield of 4% to 4.5%. I give a range because without doing the work on all individual companies it’s hard to know exactly how much to penalize the FCF over the last 5 to 10 years for a lack of a real economic recession. If we assume that this universe grows FCF at about 5%, a typical historical growth rate, this would imply about a ~9% Internal Rate of Return (IRR) from buying this group of companies.

So, let’s compare the following scenarios:

We invest right away at a 9% IRR

We wait for 3 years while we search for ideas, invest in Treasury Bills at a 4% annual return, and then deploy our capital in an investment that has either 9%, 12%, 14% or 16% IRR

The 9% scenario represents the case in which we search in vain for 3 years and then invest in securities with similar expected returns to what’s available today. The other three scenarios are realistic IRRs for the typical investments that I look for and believe are very reasonable to be able to find, with hard work, within the 3 year timeframe

As you can see, with these assumptions, at worst we do slightly worse than we could have done by investing right away, but have a very decent chance of doing much better despite waiting a whole 3 years. In practice, I don’t think the whole 3 years is likely to be needed, as good ideas historically have come more frequently than that, but I wanted to use that waiting period to illustrate the point.

Let’s say however, that we think ourselves to be Mr. Stock Pickens McPickens. McPickens doesn’t need to settle for mere group-average returns of 9%. He is one insightful hombre, and he is going to find that winning stock even in a tough market. That’s what he is paid to do, darn it!

Maybe. Or maybe McPickens makes a mistake. In his desire to find high returns and look smarter than his peers, he gets too clever for his own good.

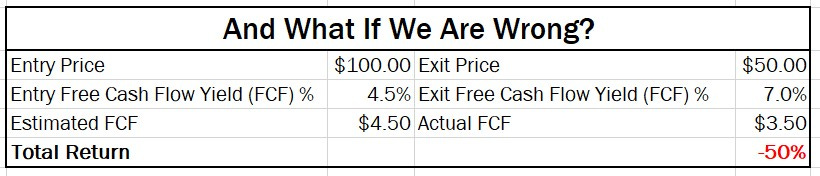

Let’s say he buys a quality company at the average FCF yield of 4.5% that is available today. McPickens has a very fancy argument, supported by reams of data and lots of field research that makes him believe this is a high-growth business. A compounder, perhaps the next Costco or Amazon!

Except that such companies are exceedingly rare. So, let’s say that this time the market got the better of McPickens, and he was actually a bit too optimistic on the starting FCF of the business. Perhaps he didn’t fully appreciate the cyclical boost to current profits. Also let’s assume that while the business he picked is still quite good, it ended up being mature and couldn’t generate much more than low single-digit future growth. That is the growth of a typical mature business, after all.

So what would McPickens’ visionary bravery do to the capital he invested if he were wrong?

He would lose 50% of his money.

By the way, while McPickens is not a real person, he is inspired by my voracious reading of many investors’ letters and investment theses. And perhaps by some of my own McPickens-like mistakes of the past. In investing, experience needs to build both confidence and humility. The former without the latter is just unwarranted hubris.

If you liked this article, please “like” and share this article. If you are interested in learning more about the investment process at Silver Ring Value Partners, you can request an Owner’s Manual here.

About the author

Gary Mishuris, CFA is the Managing Partner and Chief Investment Officer of Silver Ring Value Partners, an investment firm that seeks to apply its intrinsic value approach to safely compound capital over the long-term. He also teaches the Value Investing Seminar at the F.W. Olin Graduate School of Business.

Always delivering value. Hope you enjoy the Berkshire Annual Meeting!